Researchers

Yinchi Chen

Yufei Zha

Shijie Cai

Faculty Advisor

Zhenyu Cui

Dr. Christian Homescu

Abstract

The research aims to create an effective testing framework for investment strategies and portfolios in QWIM. The performance is evaluated by various testing methods, including back testing, bootstrapping, scenario testing, and in-sample out of sample testing, to assess their ability to predict the market. Ultimately, all methods are integrated to develop a comprehensive testing framework.

Result

Different testing methods such as Portfolio Testing, Scenario Testing, BackTesting, and Bootstrapping. The formula used in Portfolio and Scenario testing is shown below with different weights for different variables.

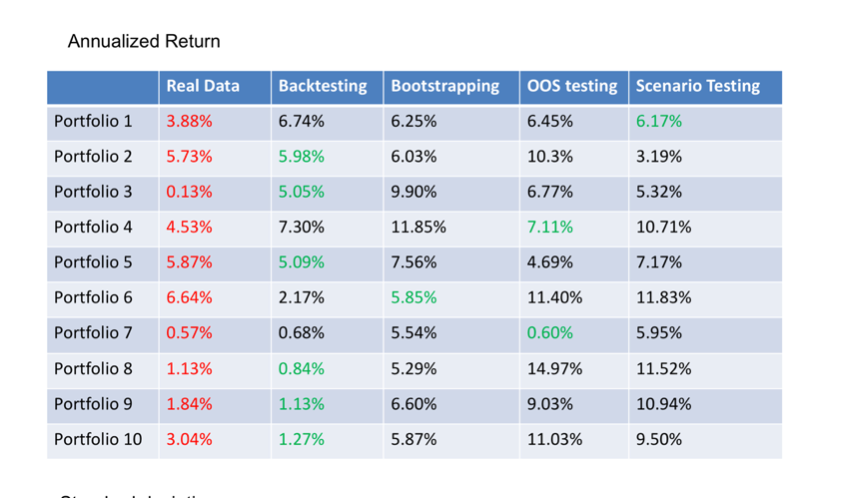

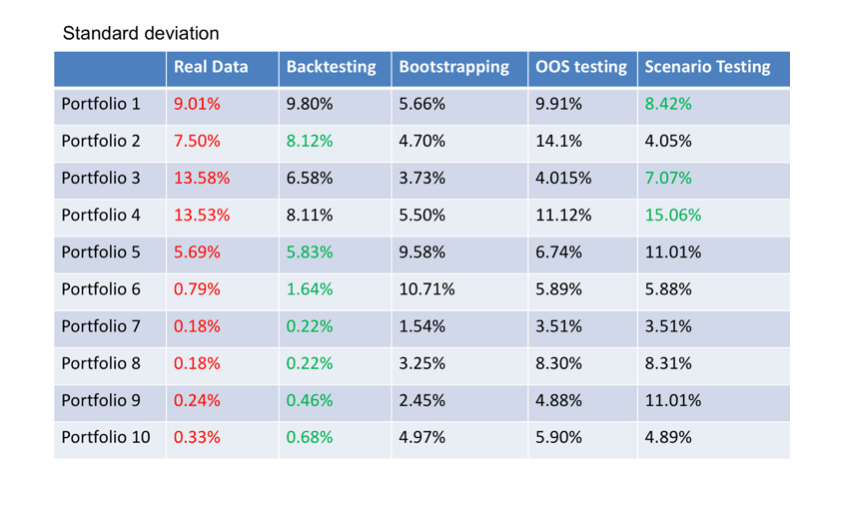

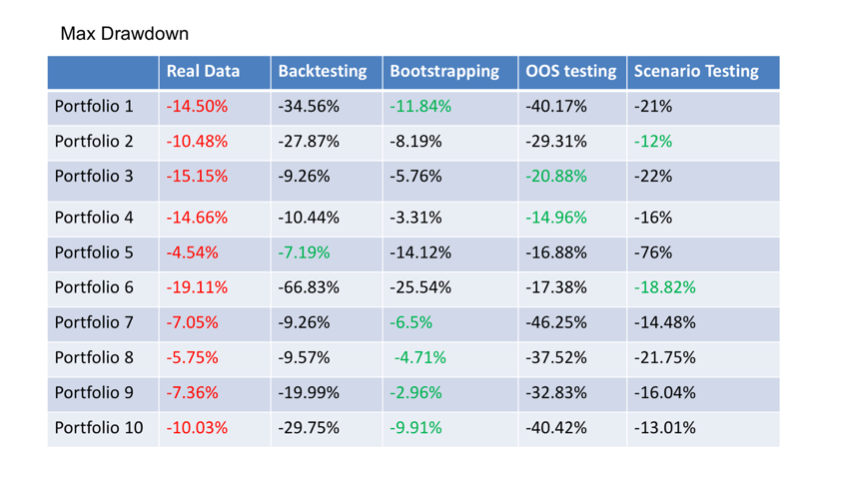

The test framework helps determine which method generates data that is closest to real historical data. 10 portfolios are tested to obtain 4 indicators: Sharpe Ratio, Annual Return, Standard Deviation, and Max Breakdown

The results of all 4 indicators against different testing methods are as follows

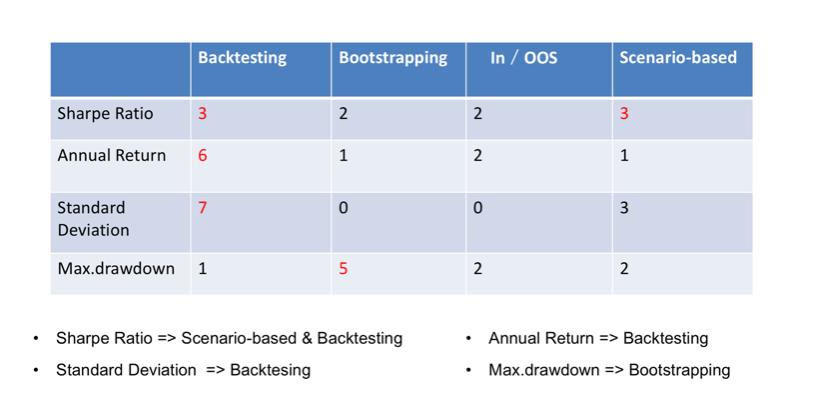

By merging together all frameworks, following is concluded:

Conclusion

The research finds out that based on the existing portfolios available, backtesting is an efficient method in predicting Sharpe ratio, annual return and standard deviation. Bootstrapping works well when it comes to the prediction of Max.drawdown, and scenario-based testing should be preferred when it comes to predicting Sharpe ratio.