On Wednesday, May 7th, the Hanlon Financial Systems Center hosted the awards ceremony for the annual High Frequency Trading Competition (HFTC). This unique event brings together teams from around the world to develop and deploy trading strategies and algorithms in a high-frequency setting. The competition was facilitated by Matthew Thomas, a first-year Ph.D. student in Financial Engineering, and overseen by Dr. Ionut Florescu, Director of the Stevens Hanlon Lab.

The competition was conducted on Stevens' proprietary SHIFT platform—a realistic trading simulation environment that allows participants to place orders, interact with a dynamic order book, and retrieve intraday data. This level of granularity enables competitors to design and refine market-making strategies far beyond the capabilities of simulations that rely on daily or monthly data. This simulation advantage makes the HFTC a one-of-a-kind experience exclusive to Stevens.

Spanning five weeks, the competition presented five distinct trading scenarios. The first three stages were based on historical market data:

- Day 1: “Up and Down Day” — featured large intraday price swings.

- Day 2: “Peak Swing Day” — reflected days with the greatest range between high and low prices.

- Day 3: “High VIX Day” — simulated extreme market volatility.

The final two stages were powered by agent-based simulations on the SHIFT platform:

- Day 4: “Zero-Intelligence Day” — featured randomly trading agents to mimic unpredictable market behavior.

- Day 5: “Reinforcement Learning Day” — involved 14 reinforcement learning agents that adapted to participant strategies, creating what facilitator Matthew Thomas called the “Day of Extremes,” where teams experienced significant wins or losses.

In preparation for each round, teams were given approximately one week to test and fine-tune their algorithms in simulated environments. This practice period allowed them to iterate on their strategies and adapt to new challenges.

The 2025 competition marked a milestone: for the first time, international participants competed alongside Stevens students. Taking first place was Team Clocksense Trading, comprised of Shubham Nahata and Aayush Mittal from BITS Pilani in India. Despite working across time zones, technological limitations, and not having formal financial backgrounds, they impressed the audience with their discipline and approach: “Consistency. Simplicity. Execution.” In their Zoom presentation, they described the competition as akin to an internship, thanking the organizers for a transformative experience.

Second place went to Team Spread Snipers, composed of Stevens students Sharif Haason, Scott Henriquez, Akbar Pathan, and Saugat Shrestha. They employed a market-making strategy and noted how the hands-on format helped them learn and adapt quickly—especially during the agent-based trading days, where they posted strong results.

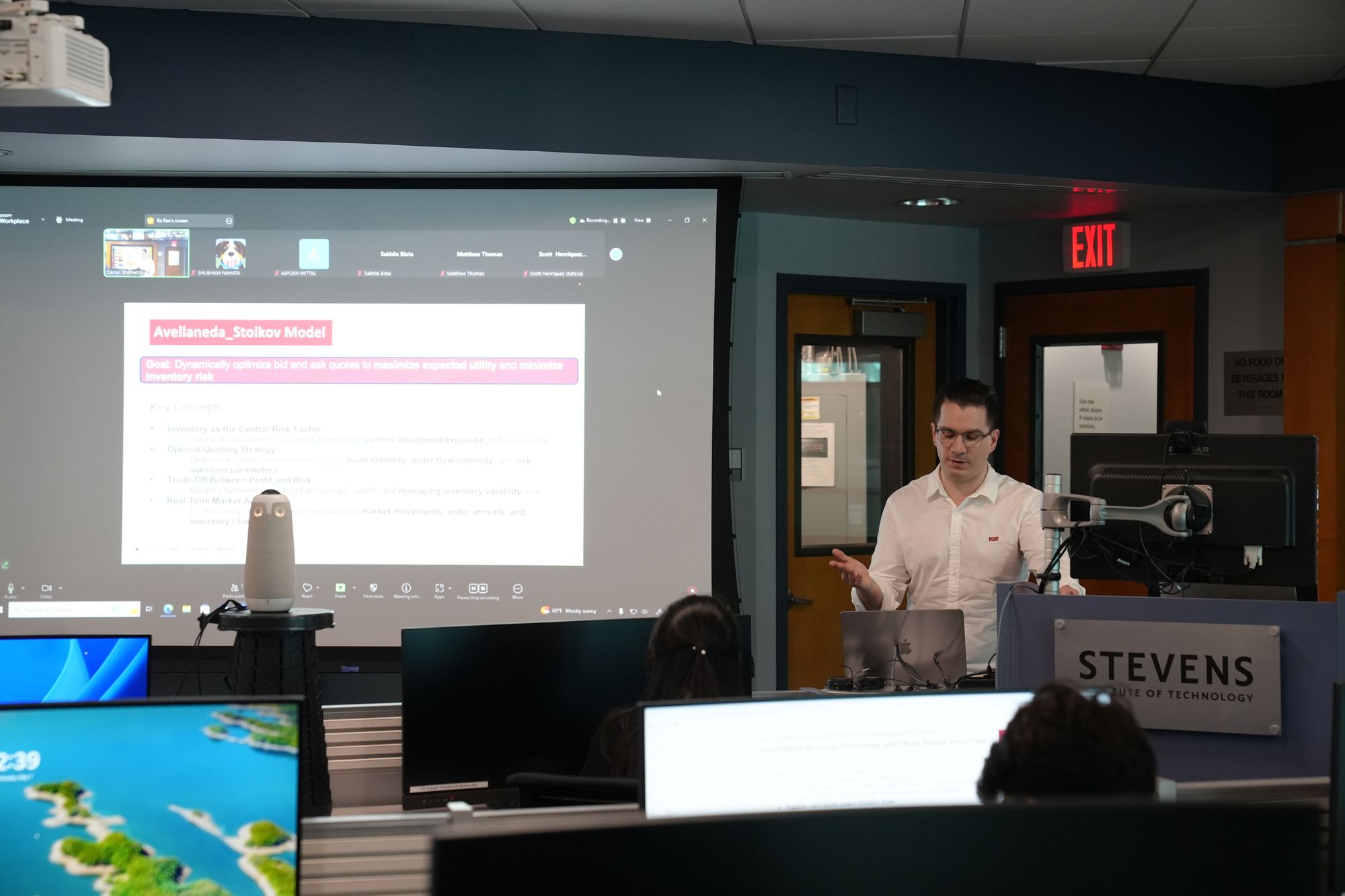

Third place was awarded to Team Money Never Sleeps, made up of Stevens students Bence Marton and Ke Ren. Their strategy leveraged the Avellaneda-Stoikov Model, which dynamically adjusts bid-ask quotes to optimize expected utility and manage inventory risk.

A total of 22 teams participated in this year’s competition. Although not all teams completed the challenge, every participant expressed gratitude for the opportunity to apply classroom knowledge in a live simulation environment.

On behalf of the Hanlon Financial Systems Lab, we extend a special thank you to Matthew Thomas for organizing an exceptional competition. His preparation began in the Fall 2024 semester, and his dedication to ensuring a smooth and engaging experience for all teams was instrumental to the event's success. We would also like to recognize Adam Moszczynski for his significant contributions to the set-up and management of the competition.

Our sincere thanks go as well to the support team—Daniel Shemetov, Ishan Kakodkar, Remoun Salib, Dan Lui, and Dominic Magats—who provided valuable one-on-one guidance to the participating teams throughout the competition.

Finally, a special thanks to Zheng Xing and the IT team for their assistance in setting up the technical infrastructure that made the competition possible.

Congratulations to all the winners—and to every participant who invested their time and creativity into developing high-frequency trading algorithms!